Marketing for monopolies

The Water Report

17 December 2018

Tags

This article was first published in The Water Report

Now that the business plans for 2020-25 have been submitted by the water companies, the vision and high-level target outcomes in their Performance Commitments (PCs) are clear. The focus now is shifting to how they will meet all these commitments, including getting to the right starting point by April 2020.

It will be critical for companies to take every opportunity to enhance performance. That means taking a new look at how water companies create value, both in the traditional value chain and in new areas, to identify both gaps and opportunities to deliver more. All that will have to include a relentless and consistent focus on delivering customer value and an ability to respond dynamically to their changing expectations and behaviour.

C-MeX and PCs

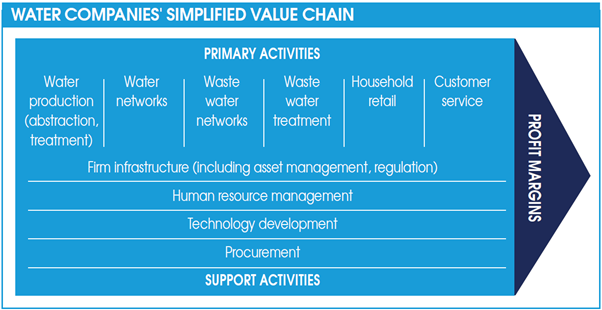

The water companies’ current approach typically follows the simplified value chain illustrated below.

Compared to a traditional value chain view, one primary activity missing from the water company chain is marketing and sales, which in the traditional value chain would exploit competitive advantage, build customer loyalty and drive growth in market share. This omission is not surprising because household customers do not have a choice of water or sewerage service provider, so while some marketing activities do take place, they are not considered primary activities. In today’s customer focused world, this simplified value chain view combined with less mature marketing and sales capabilities are key barriers to companies becoming truly customer-focused in their core activities.

A failure to address this in a rigorous and focused way will lead to sub-optimal outcomes during the next price review period, not least in the form of lower C-MeX rewards (or even C-MeX penalties). Failing to engage customers more fully on new value propositions will limit customer participation and lead to lost opportunities to contribute to the achievement of the PCs which are related to demand such as leakage, per capita consumption and sewer flooding.

Other problems in this simple value chain view are that it identifies the drivers of cost and value in a linear way which transforms inputs into output products. However, this does not fully describe the different ways in which water companies create value today, and crucially it is wholly inadequate to describe how they will need to create value tomorrow.

A simple and current example of this problem is household metering which typically sits in the household retail part of the value chain. However, metering as a customer value proposition is presented very differently across water companies and this results in varying levels of meter penetration and customer willingness to move to metered tariffs. Equally, it misses the point that household metering also creates value in other parts of the chain, for example in terms of helping to improve identification and quantification of leakage. If companies do not quantify these benefits across the entire organisation they will not focus on developing customer value propositions which will deliver them fully.

Redefining marketing

The response to these challenges needs to be twofold. First, water companies should look at how they can focus marketing and sales as primary activities which deliver value directly. To do this, typical marketing and sales objectives should be re-defined in the context of water companies’ strategic objectives and PCs.

For example, the traditional marketing and sales objective to exploit competitive advantage could be re-defined to exploit innovative customer value propositions and to keep pace with changing customer expectations. The measure of success would be higher C-MeX scores and strong performance against the UK Customer Service Index, particularly from customers who have had contact with the water company.

Building customer loyalty is another typical marketing and sales objective which should be redefined. The re-defined objective could be to create customer advocates across both core service provision and wider strategic objectives such as support for vulnerable customers, driving sustainability and access to amenities. Success would again be measured through higher C-MeX scores, across both customers who have had contact with the water company and those who have not.

Finally, another typical marketing and sales objective is to drive growth in market share. This should be re-defined as growing the customer base served by different customer value propositions. Outcome-based customer segmentation should drive an enhanced understanding of the customers’ world, and how the water company can shape its value propositions to enhance that world. The measure of success here would be sustainable increases in the take-up of new services such as metered billing and online account management, and in levels of customer participation, for example supporting the achievement of PCs such as water efficiency, leakage, and sewer flooding.

Water companies are already taking some of the actions required to address these points. Indeed, the business plans submitted to Ofwat for PR19 contain details of strong ambitions amongst companies to create additional value. However, the ambition in those business plans must now be translated into primary marketing and sales activities which are fully coordinated across the organisation ensuring it has a single view of the customer; designed to evolve dynamically in response to changing customer expectations; and data driven, using accurate and well managed customer data obtained both by the water company directly and via appropriate third parties (for example, credit reference agencies, government organisations, other consumer groups).

Networks not chains

The second aspect of the response to these challenges is to understand the opportunities to deliver better outcomes by categorising water company activities using additional types of value creation rather than simple value chains. These could include value networks or value webs, where value creation is not limited to the core products/services in the traditional value chain view, but is based on the utilisation of the water company’s assets by an expanded range of customers.

Examples of the value network approach already exist. Ofwat is driving disaggregation of production and distribution through separate price controls and has already separated non-household retail functions through the establishment of the non-household retail market. This has begun to reduce the dominance of the traditional value chain and helps create the environment for value networks, not least because it introduces a new range of potential customers and suppliers, and a new range of services to be provided by the water companies using their assets.

In addition, some companies are starting to deliver circular economy innovations, which create value through the re-use of waste or by-products. These are often delivered with major customers and are good examples of value network-oriented approaches ouside the core activities. Examples of value networks involving end customers include Yorkshire Water’s ‘Fats to Fuel’ recycling project in Bradford. This creates value for customers and communities through the collection of waste fat which avoids sewer blockages, and which is then is sold for use in renewable energy generation. And Severn Trent Water’s ‘Uber for leaks’ platform. This created value particularly for students (who are not necessarily bill paying customers and are therefore a new type of ‘customer’) who signed up to participate in a leak locator initiative on a pay-per-leak basis.

There is a clear opportunity to explore and develop value networks further and involve all types of customers in a more consistent and sustainable way. The critical measure of success is that these value networks deliver value for customers while contributing to the water company achieving its performance commitments.

The challenge now is to maximise the potential for these value networks to be identified, developed, deployed and delivered at scale. This will require:

- A wider definition of customers to include all parties who participate in services offered by the water company, not just bill payers.

- The definition of consistent customer segmentation based on what customers value. This will identify which customers should be targeted for different services, and to enable delivery against different marketing and sales objectives.

- Customer research and a customer-led design thinking approach for new or enhanced services.

- The definition of requirements for coordination of the delivery of customer value across the entire organisation, and the organisational agility to meet changing customer expectations and behaviour changes.

- A detailed understanding of the contribution that these approaches will make to the goal of achieving high C-MeX scores and strong performance in other PCs.

With a more comprehensive and coordinated understanding of the value that can be delivered both to customers and in partnership with customers, water companies will be better placed to understand the transformation they need to undertake to deliver successfully in AMP7 and beyond. Once the objectives for this transformation are clear they will be able to understand what capability they need and be able to implement the right operating model and organisational design to deliver it in a sustainable way as customer expectations and behaviours continue to evolve.

Companies who do this now will differentiate themselves in terms of customer-centricity, enhancing outcomes against their PCs including C-MeX and demonstrating real commitment to delivering on their social contract.

Explore more