Evolving the regulated asset business – small steps or giant leaps?

Utility Week

06 November 2018

Tags

The article first appeared in Utility Week

As “First Man” is currently reminding us, Neil Armstrong conquered the paradox of turning one small step into one giant leap. As regulated asset businesses look to the next stage of their evolution, it is clear they face a similar challenge. Regulators, politicians, policymakers and the public are demanding more of these businesses in a future world that is a giant leap from the current position. Regulated asset businesses are naturally cautious, engineering-focused and evidence-based, more accustomed to taking small steps so how can these businesses make the necessary changes?

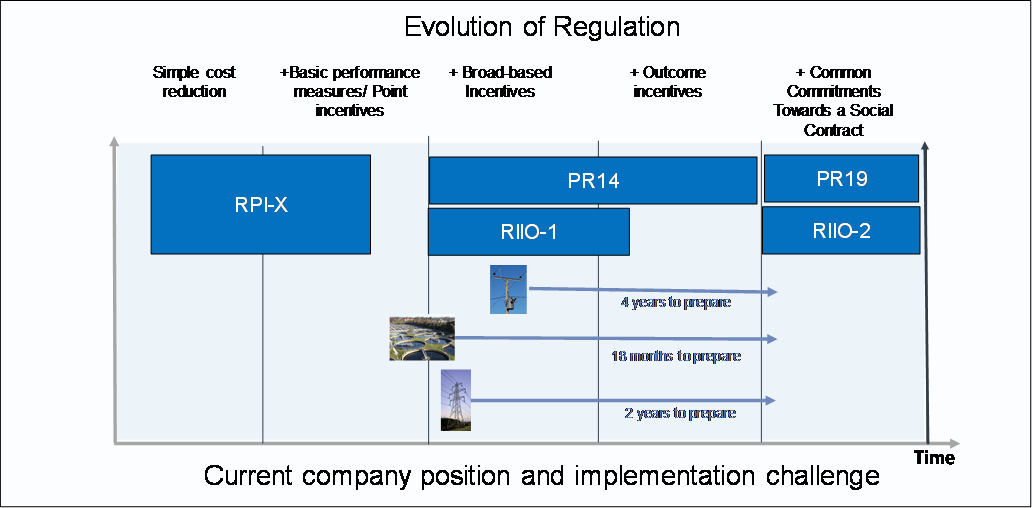

Answering that question requires an understanding of the evolution of regulation and associated political and public pressure, where the businesses are and the scale of the challenge. The diagram below maps out these factors.

Regulation has developed significantly since its inception post-privatisation. The initial RPI-X regimes focused on cost reduction and point incentives such as the interruptions incentive in electricity. These were effective in driving cost out of the businesses, reducing costs to customers and improving baseline performance. They were far less effective at delivering an improved customer experience, ensuring asset investment was correctly focused and encouraging innovation. The subsequent regimes aimed, to an extent, to address these issues.

RIIO1, across gas and electricity, distribution and transmission, introduced a more sophisticated output-based regime, attempting a more holistic approach and complex incentivisation model, with incentives such as the broad-based measure of customer satisfaction. Stakeholder engagement was given greater prominence but centred around the companies view of what was right for customers rather than directly engaging in true customer centricity. It also “tipped its hat” to social obligation, centred on vulnerable customers and supporting the transition to the low carbon economy.

PR14, in the water industry, trumped this and aimed to move to an outcome, as opposed to output model. Under this model, companies set their own outcomes and measures and introduced a radical approach to give customers a greater say in those success factors and the costs required to drive them.

Both these regimes had merit and have undoubtedly achieved better outcomes for customers, but that success has been almost completely overshadowed by the debate on corporate structures and financial rewards. While regulatory policy was focused on protecting the interests of customers through greater efficiency and creating a flexible environment in which the right longer term decisions would be made, some owners were focused on capital structures and financial engineering.

This was exacerbated by the setting of the weighted average cost of capital (Wacc), which, with hindsight, is generally recognised as having been high in a post-financial crisis world of sub 1 per cent interest rates. This has led to the development of a more challenging political climate where, after 30 years of post-privatisation progress, re-nationalisation is openly being discussed.

Regulators are responding to this. PR19 sets out common commitments that will enhance regulatory scrutiny, a much lower Wacc is clearly signposted and there are clear pressures on corporate structures in the water industry. The RIIO2 regimes are further away, but Ofgem is very clearly addressing the same issues.

Companies have made significant progress in responding to these changes but it is difficult to avoid the conclusion that they are continually having to catch up with the regulatory and political pressures.

Big challenges

The network companies have achieved substantive cost savings and trimmed down to leaner efficiency-focused businesses, but now need to embrace technical, organisational and commercial innovation to facilitate the emerging world of distributed energy. They, arguably, have four years to establish this and forward-thinking companies are already planning for the challenge of a lower Wacc, greater cost and customer demands and a more innovative environment.

The water industry is facing the biggest challenges. Although PR14 was a more forward-looking regime, and has stimulated some efficiency gains, the scale of change required to position the companies for the demands of PR19 is that much greater. Water companies, cover the full value chain from source to customer including retail with added interfaces and associated complexity. The water industry now faces its own trilemma of the most significant change in the shortest timescale, whilst bearing the brunt of the political pressure.

How then should companies meet these new challenging targets and ensure they can deliver for their customers, be soundly financed and provide an acceptable shareholder return? Historically, regulated asset industries are naturally attuned to playing a long game, but it may now be time to turn that on its head. Business as usual and gradual evolutionary change will not be enough, and companies will need to address four key areas to bring about the necessary transformation.

The first of these is to recognise and embrace the need for fundamental change to raise performance to the next level and beyond. Doing more of the same in the same way will not help with the “giant leap” that is needed. Companies will need a refreshed vision and a revitalised, value for money proposition for each customer if they are to remain relevant into the future.

Secondly, there is a need to rapidly embrace digital and innovation. We can all see the havoc that digital is supposedly wreaking on the high street, though it is really consumers who are wreaking havoc, by changing their needs and taking their business elsewhere. Digital is just an enabler and water companies need to understand how it can enable their business, what other innovations can create a step-change and how they can adopt an enduring innovation culture. The government has also launched a consultation on how regulation can enable cross-sector collaboration and how to stimulate innovation which will allow further debate on new approaches, in addition to the strengthening of the UK Regulators’ Network.

Thirdly, companies should embrace agile working. Confronted with the need for change, the temptation is to reach for the transformation manual, but major programmes are fraught with challenges and industries with a focus on the long term tend to create slow-moving transformations, hampered by legacy systems and processes. Agile transformation is a much better approach and our own research has shown that agility is critical to strong company performance.

Last, and perhaps most importantly, companies will need to change the cultural and stakeholder conversation. That means putting the customer and society at their heart and understand their world and needs and develop the capabilities to respond dynamically to the changing external environment.

Now is the time to protect our future prosperity and create a new social contract that re-engages customers, government, regulators and the environment. Our regulated asset industries must lead this change if we are to make this giant leap.

Explore more